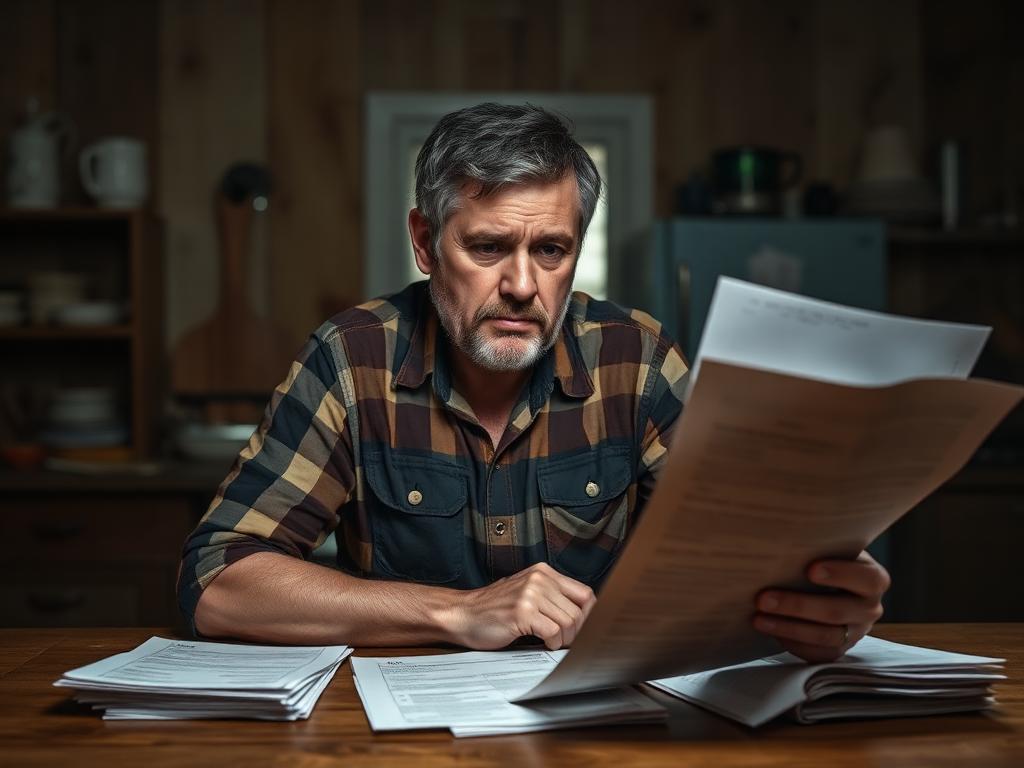

America's agricultural heartland is facing its most severe financial crisis in decades. As 2025 unfolds, small and family-owned farms across the nation are buckling under the combined pressure of record-high debt levels, collapsing commodity prices, and an unprecedented wave of consolidation by corporate investors and institutional buyers. What was once the backbone of American agriculture—the small family farm—now finds itself fighting for survival.

The Crisis by the Numbers

Farm Bankruptcies Surge 38%

Chapter 12 filings reach highest level since 2012

$520 Billion in Total Debt

All-time high for U.S. farm sector

Corn Prices Down 45%

From 2022 peaks, devastating Midwest operations

12,000+ Farms Lost Annually

Consolidation accelerates across all regions

According to the U.S. Department of Agriculture, farm debt has reached an unprecedented $520 billion, with no signs of abating. The debt-to-income ratio for American farmers now sits at levels not seen since the devastating farm crisis of the 1980s, when thousands of operations went under.

A Perfect Storm of Economic Pressure

The crisis stems from multiple converging factors that have created a financial vise grip on small agricultural operations. First, commodity prices have plummeted from their pandemic-era highs. Corn, which peaked at over $7.50 per bushel in 2022, now trades below $4.20. Wheat prices have fallen similarly, while soybean prices remain stubbornly low despite strong export demand.

Meanwhile, input costs remain elevated. Fertilizer prices, while down from 2022 peaks, still run 60% higher than pre-pandemic levels. Diesel fuel, essential for running farm equipment, continues to fluctuate with global energy markets. Equipment costs have soared—a new combine harvester that cost $400,000 in 2019 now carries a price tag exceeding $650,000.

The Cost-Price Squeeze

- Operating loans now carry interest rates of 8-10%, up from 3-4% in 2020

- Labor costs have increased 25% due to worker shortages and wage pressure

- Land rental rates remain at historic highs, with no relief in sight

- Insurance premiums have doubled in many regions due to climate-related losses

The result is a devastating profit squeeze. Many operations that showed positive margins just three years ago are now operating at a loss. Small grain farmers in the Midwest report losing $50-$100 per acre on their 2024 crops. Cotton growers in the South face similar losses, with no improvement projected for 2025.

The Great Consolidation: Who's Buying

As small farmers struggle, deep-pocketed buyers are circling. The farmland consolidation wave of 2025 represents the most significant transfer of agricultural land ownership in American history. Three distinct buyer categories are driving this transformation:

Institutional Investors

Private equity firms, pension funds, and sovereign wealth funds have deployed over $15 billion into U.S. farmland acquisitions since 2023. These entities view agricultural land as an inflation hedge and stable long-term investment, often outbidding family farmers by 20-30% or more.

Corporate Mega-Farms

Large agricultural corporations continue expanding their landholdings, leveraging economies of scale that smaller operations simply cannot match. These mega-farms operate on margins impossible for family operations, using advanced technology, bulk purchasing power, and vertical integration.

High Net Worth Individuals

Wealthy individuals seeking portfolio diversification and tax advantages are acquiring farmland at unprecedented rates. Tech entrepreneurs, hedge fund managers, and foreign nationals see American farmland as a safe-haven asset in an uncertain global economy.

The average price paid for farmland sales has increased 23% over the past two years, even as farm incomes have declined. This paradox reflects the investor-driven market, where buyers value land for its appreciating asset value rather than its agricultural productivity. For struggling farmers, this creates a difficult choice: sell now at peak prices while facing mounting losses, or hold on and risk complete financial collapse.

Regional Impacts: No Area Spared

While the crisis affects all regions, certain areas face particularly acute challenges:

The Midwest Corn Belt

Iowa, Illinois, and Indiana have seen the highest absolute numbers of farm bankruptcies, with small grain operations particularly vulnerable. Multi-generational family farms that survived the 1980s crisis now face their greatest test.

The Great Plains

Kansas, Nebraska, and the Dakotas struggle with persistent drought conditions layered on top of economic stress. Wheat and cattle operations face double-digit income declines, forcing accelerated land sales.

The Cotton South

Texas, Georgia, and Mississippi cotton growers battle both low prices and increasing production costs. Many operations are switching to less labor-intensive crops or selling outright.

California's Central Valley

Water scarcity compounds financial stress, with many farmers choosing to sell water rights along with land to maximize proceeds. Permanent crop operations face particularly difficult decisions.

Political Response and Policy Debates

The Trump administration has faced mounting pressure to address the crisis. Government aid to farmers reached $32 billion in 2024, approaching levels seen during the COVID-19 pandemic. However, this assistance primarily flows to larger operations, with small farms receiving proportionally less support.

Congress debates several proposed interventions: expanded crop insurance subsidies, low-interest loan programs for struggling operations, and restrictions on foreign and corporate farmland ownership. However, political gridlock has prevented meaningful legislation from advancing. Meanwhile, state-level responses vary widely, with some states implementing modest restrictions on non-resident land ownership while others take no action.

The Food Security Question

Agricultural economists warn that the consolidation wave raises serious food security concerns. As production concentrates in fewer hands, the agricultural system becomes less resilient to shocks. The COVID-19 pandemic demonstrated vulnerabilities in concentrated food systems—a lesson that risks being forgotten as the crisis accelerates consolidation rather than reverses it.

What This Means for Landowners

For agricultural landowners facing this crisis, difficult decisions loom. Many farmers find themselves asset-rich but cash-poor—sitting on land worth millions while operating accounts run empty. The question becomes not if to sell, but when and to whom.

Those who choose to exit face a complex marketplace. Institutional buyers offer quick closings and cash deals but may lowball on price. Local farmers seeking to expand often can't compete financially but may offer intangible benefits like keeping land in agricultural use. For those who need to sell vacant land quickly, understanding market dynamics and having professional representation becomes crucial.

Key Considerations for Sellers

- Timing matters: Current prices remain historically high despite farm income stress. Waiting could mean missing the peak.

- Tax implications: Capital gains treatment and potential policy changes make professional tax advice essential.

- Buyer vetting: All-cash offers aren't always the best deals. Financial strength, closing certainty, and reputation matter.

- Legacy preservation: Some sellers prioritize keeping land in agricultural use over maximum price, requiring careful buyer selection.

Looking Forward: No Quick Fix

Agricultural economists see no near-term relief for the current crisis. Commodity prices are expected to remain subdued through at least 2026, with global oversupply likely to persist. Interest rates, while potentially declining slightly, will remain elevated by historical standards. Input costs show no signs of returning to pre-pandemic levels.

The consolidation trend appears unstoppable without dramatic policy intervention—intervention that currently lacks political will or consensus. The American agricultural landscape of 2030 will likely look vastly different from today, with fewer, larger operations controlling greater market share.

For the small family farm that has defined American agriculture for generations, the outlook is grim. While some will survive by finding niche markets, adopting regenerative practices, or serving local food systems, the majority face an inevitable choice: adapt radically, merge with larger operations, or exit entirely.

The Bottom Line

The 2025 farmland crisis represents a historic inflection point for American agriculture. As small farms buckle under financial pressure and institutional investors reshape the ownership landscape, the very character of rural America hangs in the balance. For landowners caught in this transformation, the path forward requires clear-eyed assessment of options, professional guidance, and difficult decisions about legacies built over generations. The American farm as we've known it is being fundamentally rewritten—and the new chapter is being written right now.

Facing Tough Land Decisions?

If you're considering selling your farmland or vacant property, we provide fast, fair offers with transparent pricing and quick closings.

Get Your Free Land EvaluationNo obligations. Professional guidance through every step.